Ontario homeowners are being slowly but surely priced out of the insurance market — and the province’s financial regulator is standing on the sidelines.

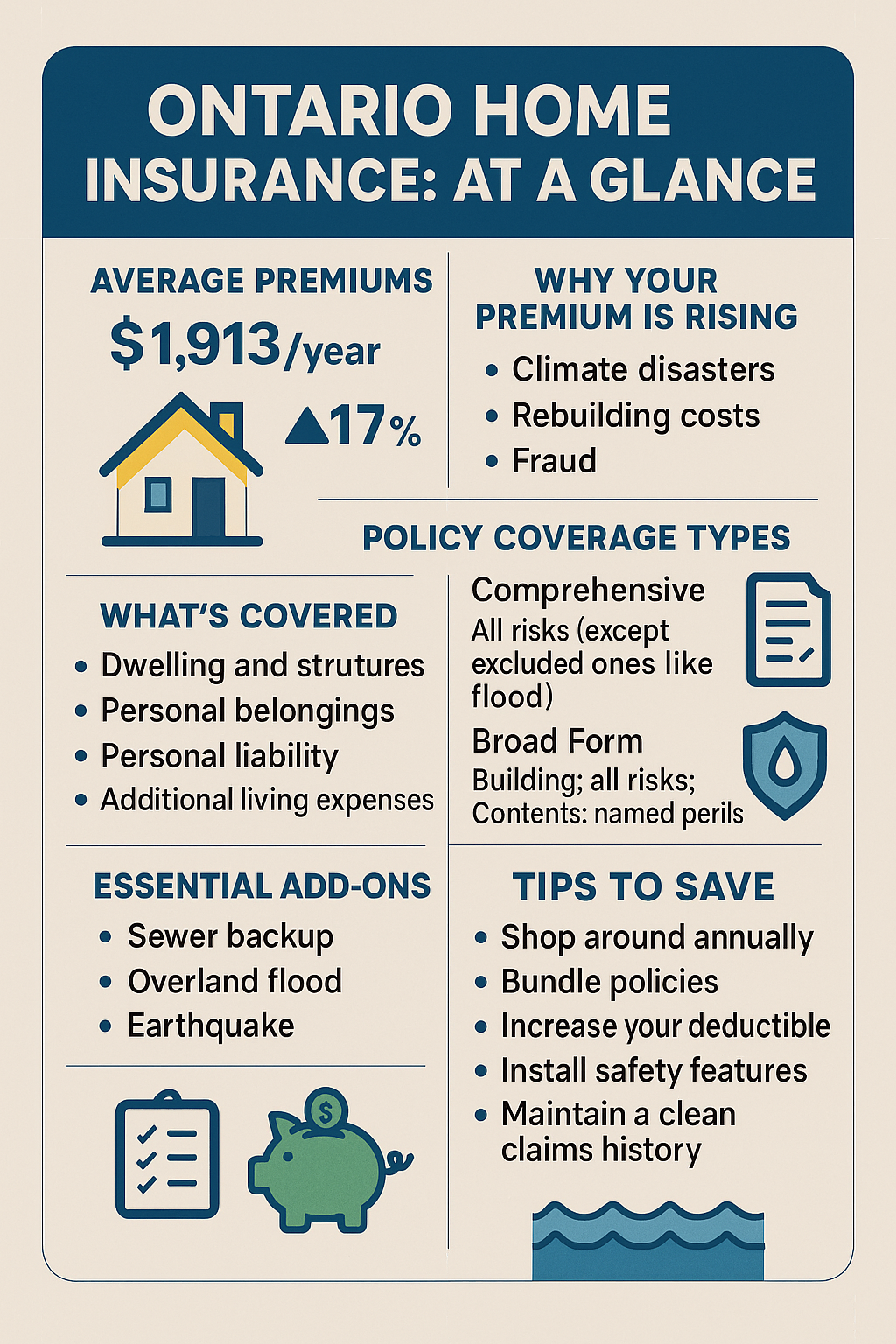

Between 2014 and 2024, home insurance premiums in Ontario surged by a staggering 84%. Over the same period, general inflation rose just 28%, according to Statistics Canada. That’s not just inflation at work — that’s a crisis.

What’s fueling this massive increase? Climate change, plain and simple. More frequent floods, windstorms, wildfires, and other extreme weather events are battering communities and insurance companies alike. The result? Skyrocketing premiums, particularly for those living in higher-risk areas.

But here’s the real problem: Ontarians have no idea how bad it’s going to get — or whether anyone is doing anything about it.

Unlike the auto insurance market, where the Financial Services Regulatory Authority of Ontario (FSRAO) regularly releases detailed reports and statistics, home insurance remains a black box. Consumers see their bills going up every year with little to no explanation. There’s no transparency, no forward-looking analysis, and certainly no clear strategy to address the growing affordability problem.

Now, a climate advocacy group, Investors for Paris Compliance, has filed a formal complaint urging FSRAO to act. They’re asking for the regulator to investigate the trends driving home insurance rates, especially as they relate to climate impacts and long-term affordability.

It’s a reasonable — even necessary — request.

The group also raises another important point: many of the very insurers passing on climate-related costs to consumers are still investing in fossil fuels, the root cause of the crisis. Meanwhile, they’re lobbying for government-backed insurance safety nets for high-risk properties — essentially asking taxpayers to bail them out while they continue to fuel the fire.

This is the kind of systemic contradiction that demands regulatory oversight. Why should insurers be allowed to profit off climate risk while avoiding accountability for contributing to it?

FSRAO has a responsibility to protect not just the stability of Ontario’s financial services sector, but also the people who rely on it. That includes ensuring consumers aren’t left in the dark — or worse, left unprotected — as climate change makes insurance less accessible and more expensive.

If the regulator can track auto insurance trends, it can do the same for home insurance. If it can monitor risk, it can also plan for resilience. What’s missing isn’t capability — it’s will.

Home insurance is becoming unaffordable for too many Ontarians. Without action and transparency from FSRAO, the problem will only get worse.

It’s time for the regulator to step up.