The Bank of Canada’s latest interest rate cut may feel like a breath of fresh air for Canadians worn down by high borrowing costs and a sluggish economy. By lowering its overnight benchmark rate from 2.75 to 2.5 per cent, the central bank is clearly signalling that the economic headwinds—from a limping labour market to a still-unsettled trade war—can no longer be ignored.

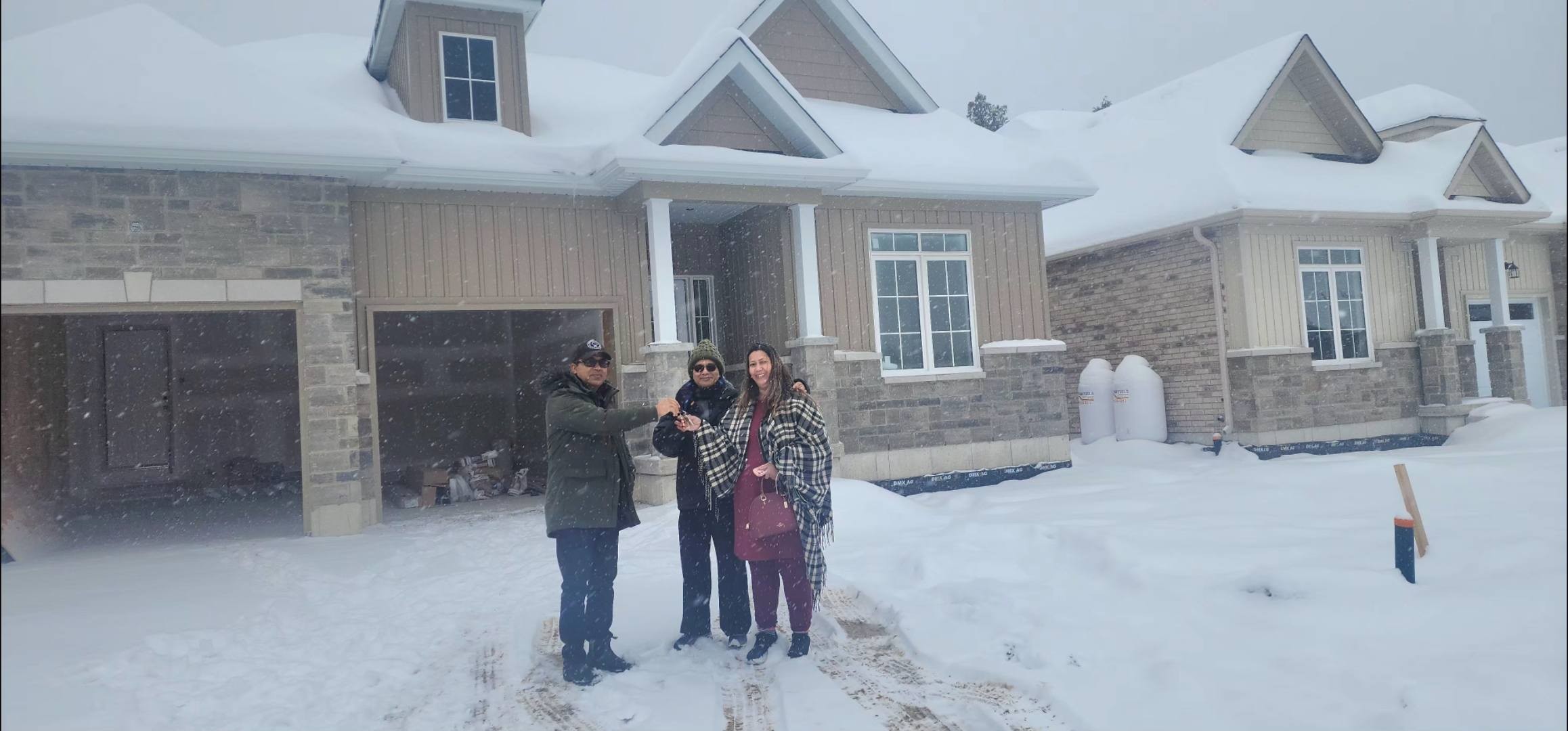

On the surface, the move looks like a gift to homebuyers and anyone carrying variable-rate debt. Lower rates typically mean cheaper mortgages and auto loans, and there’s no doubt some Canadians will seize the moment to lock in financing they might have found out of reach just a few months ago. In a housing market where affordability has been steadily eroding, even a quarter-point trim can make a difference.

But it’s worth keeping perspective. This is a cautious cut born of necessity, not exuberance. Governor Tiff Macklem underscored that reality when he acknowledged both the “soft” labour market and the trade frictions that monetary policy simply can’t fix. Tariffs with our largest trading partner continue to drag on growth and inject uncertainty, and the Bank knows it can only soften the edges, not rewrite the rules of global commerce.

The bigger question is whether this is a prelude to something more serious. While Macklem insists Canada isn’t on the brink of recession—at least under the current tariff scenario—growth has already turned negative for one quarter and is expected to limp along at roughly one per cent in the back half of the year. That’s hardly a ringing endorsement of economic health.

For would-be homebuyers or anyone eyeing a variable mortgage, the message is mixed. Yes, borrowing is a bit cheaper today, and markets are buzzing that more cuts could follow. But the same trade tensions that prompted this move could just as easily push inflation back up, forcing the Bank to reverse course.

In short, this rate cut is a prudent step, not a panacea. It might give households some breathing room and spark a few more real-estate deals, but it can’t substitute for the hard work of building a more resilient, less trade-dependent economy. Canadians should welcome the relief—but keep their expectations firmly in check.